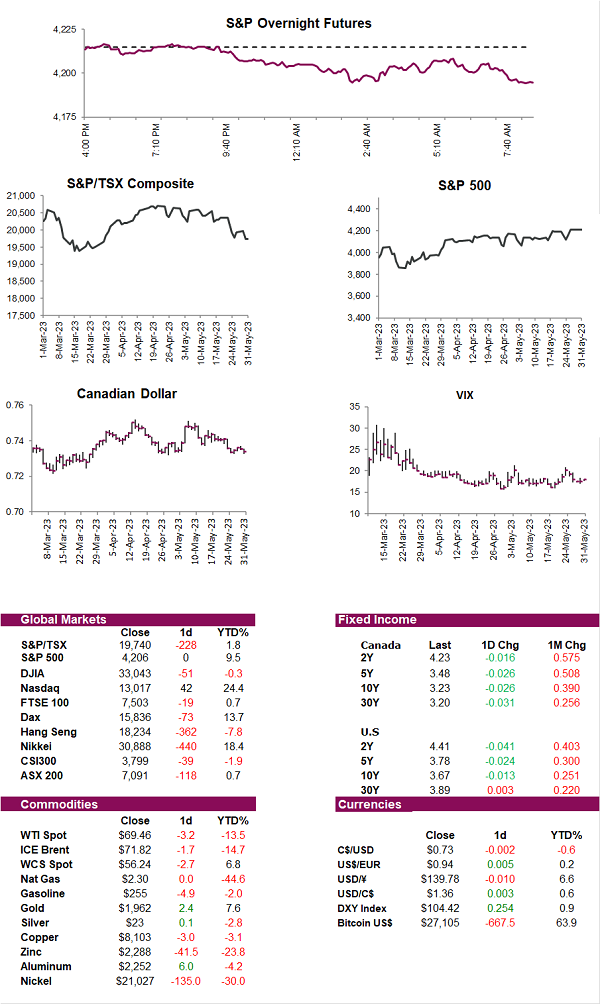

Today

North American futures slid with stocks in Europe and Asia after Chinese PMI data disappointed and as investors await debt ceiling progress. China’s growth story is starting to disappoint after soft manufacturing data added to concerns about the outlook for global economic growth at a time when central banks are still in tightening mode. Adding to concerns is the debt ceiling deal which will head to a House vote today after narrowly getting through the House Rules Committee by a 7-6 margin. With a possible default quickly approaching, today's passage is critical in getting the bill through the Senate.

Is this good news or bad news? The Canadian economy expanded at annualized pace of 3.1% in Q1 of this year, with preliminary data suggesting GDP rose 0.2% in April. Although this seems like good news, with the economy starting Q2 off strongly after a better-than-expected beginning of 2023, the likelihood of another BoC rate hike has increased. Looking closer at the numbers, household spending as well as strong exports spurred growth, raising doubts about whether the central bank has sufficiently raised interest rates. In the first quarter, household spending rose 1.5% for goods and 1.3% for services, after minimal growth in the second half of last year.

Emerging markets investors may be turning their attention towards Latin American stocks due to potentially better growth prospects. Investors have been on the lookout for emerging-market regions that show resilience and preparedness in the era of tighter monetary conditions, with some seeing that in Latin America. Stocks indexes in the region are now heading for their third month of gains, their longest winning run in more than a year, while equities in EMEA are poised for the steepest loss since September. Despite some promising signals from the region, until the Fed makes an explicit dovish pivot, any developing nation will remain vulnerable to a panicked selloff, regardless of their cheaper valuations and faster economic growth.

As part of the debt-ceiling agreement, student loan payments will resume in the coming months. The legislation would formally end the suspension that began at the start of the pandemic and would prohibit the Education Department from using its authority to extend the Coronavirus Aid, Relief, and Economic Security Act’s loan pause. If the legislation is enacted by Congress, payments will resume at the end of August. The current moratorium on payments has been extended multiple times and is reported to have cost the government about $5 billion a month. On the bright side (for those owing), the debt-ceiling deal doesn’t address Biden’s one-time forgiveness program, which would wipe out up to $20,000 in federal loans per borrower and is currently being weighed by the Supreme Court.

Consumer confidence in the U.S. fell to a six-month low, with the Conference Board’s index declining to 102.3 in May from an upwardly revised 103.7 in April. The declines come as views on the current state of the labour market and the outlook for business conditions decline, highlighting the growing uncertainty surrounding the economy. The number of respondents who expect more employment opportunities in the coming six months fell to its lowest since 2016. This figure is especially worrying to economists who have noted that the labour market has been the lynchpin supporting household spending since the pandemic began.

$1 trillion club. NVIDIA unofficially became the first chip maker to join the likes of Apple, Amazon, Google, and Microsoft in the $1 trillion dollar market cap club. Unofficial as the stock hit its high of $419.38 intraday but closed the day at $401.11, leaving it shy of the $1 trillion mark. With growing interest and adoption of generative AI, experts including executives and scientists are ominously warning about the misuse use of the technology, saying in a joint statement that “Mitigating the risk of extinction from AI should be a global priority alongside other societal-scale risks such as pandemics and nuclear war.” Over 350 people signed the statement including Open AI (the company behind ChatGPT) CEO and CTO alongside the Google CTO. The objective of the statement? To encourage an open discussion and acknowledgement of the most “severe risks” of AI. Let’s discuss.

Diversion: So close.