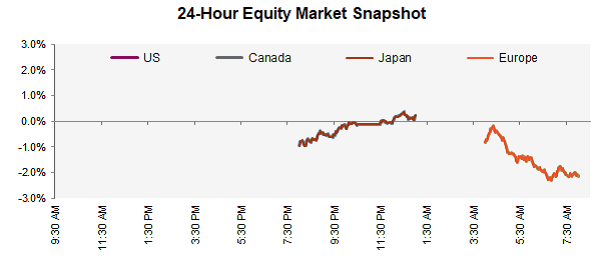

Today

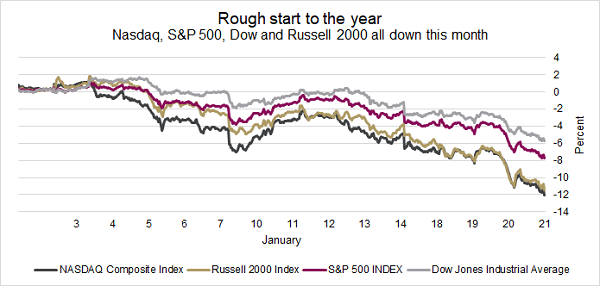

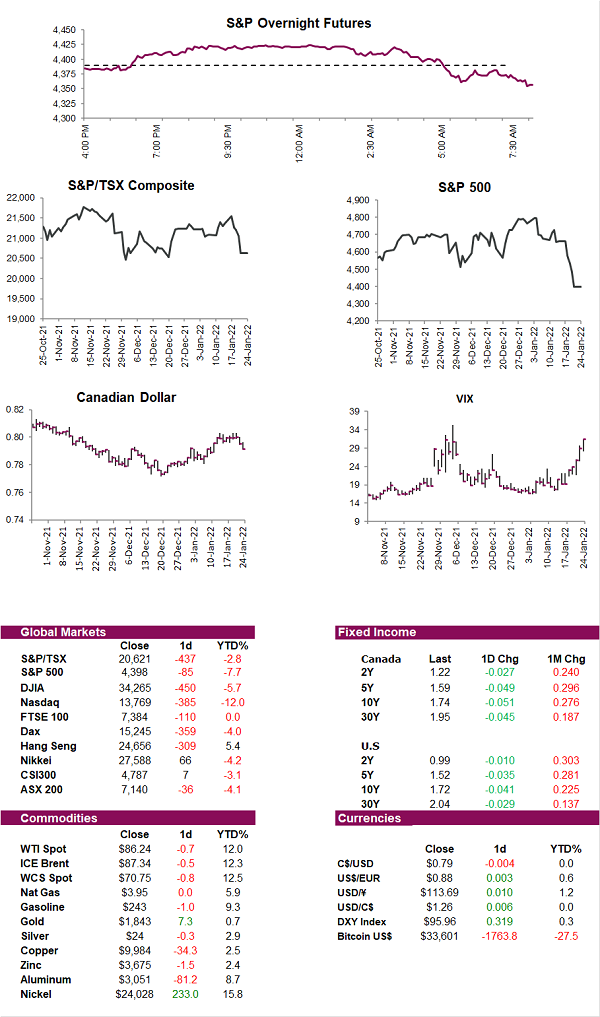

Futures fell this morning following the S&P 500′s worst week since March 2020, as investors await more corporate earnings results and a key policy decision from the Fed. It’s a busy earnings week this week with nearly half of the Dow Jones and about one-fifth of the S&P500 companies reporting. On the tech front, Apple Inc. and Microsoft Corp. Will report this week under additional pressure, with the Nasdaq 100 now on pace for its worst month since the 2008 financial crisis. A grim outlook from Netflix was the latest excuse for investors to sell tech shares causing Amazon and Meta (Facebook) to fall over 20% from their high. More than US$1.7 trillion in value has been erased from the Nasdaq 100 so far this month, with the index entering a correction after falling more than 10% from a recent peak. The industry that has powered the bull-market rally from the depths of the pandemic has recently suffered over concerns over skyrocketing valuations and a potential for slowing earnings. There are still winners out there however, as investors rotate out of growth and into cyclical more names with energy producers being the only ones in the green so far this year in the U.S.

According to a new Bloomberg report, just 9% of the roughly 1,300 ESG-focused exchange-traded funds have more than $1 billion of assets, exposing the category to large drops in assets if concentrated investors pull out. A new report highlights that most of last year’s growth was tied to financing arrangements with big investors such as pension funds making large initial investments in new ETFs, rather than organic growth. The report highlights that concentration risks are real, noting that assets dropped 91% at the iShares ESG MSCI EM Leaders after its largest holder changed allocation strategies. What was once the second-biggest exchange-traded fund investing in sustainable emerging-market companies became a shadow of its former self. In the days leading up to Christmas Eve, the iShares ESG MSCI EM Leaders ETF (LDEM) lost 91% of its investments, leaving its total assets depleted at about $69 million, compared with $803 million on Dec. 21. Only one holder of LDEM’s shares owned enough to account for such a steep outflow: Ilmarinen, the Helsinki-based pension company that made a $600 million investment in the fund when it launched in February 2020.

Despite a labour shortage in parts of the country, the Canadian government has put a hold on processing high-skilled immigrant applications. With “an estimated 76,000 applicants in the inventory” for federal high skilled worker applications, the government has what it needs to meet targets until 2023. While the current immigration plan forecasts bringing in 110,500 skilled workers next year, the department claims that the amount may be cut in half due to a lack of processing power.

Top U.S. and Russian diplomats have failed to make a major breakthrough in talks to resolve the crisis over Ukraine, although they have agreed to keep talking. This comes at a time of high tensions between Russia and the West over Russia’s massing of troops near its border with Ukraine although Moscow has insisted it has no plans to invade. The U.K. has said that Russia will face severe economic sanctions if it installs a puppet regime in Ukraine after Britain accused the Kremlin of seeking to install a pro-Russian leader there. Britain made the accusation over the weekend, also saying Russian intelligence officers had been in contact with a number of former Ukrainian politicians as part of plans for an invasion. The Russian Foreign Ministry dismissed the comments as “disinformation,” accusing Britain and NATO of “escalating tensions” over Ukraine. The U.S. State Department is now urging U.S. citizens in Ukraine to leave the country immediately, as Russia’s military buildup at the border shows no sign of dissipating.

The selloff in cryptocurrencies gained momentum this morning, with Bitcoin tumbling to a six-month low and other digital tokens seeing even bigger losses. Bitcoin sank as much as 6.6% and fell below the US$34,000 mark, continuing a six-day downturn while Ether retreated 7.6% and touched US$2,201, also the lowest since July. Crypto has come under widespread selling pressure in recent days, with traders pointing to hawkish signals from the Fed and a selloff in technology shares as reasons for traders to withdraw from risky assets. Since its all-time high in November, Bitcoin has tumbled more than 50%.

Diversion: Does yesterday’s Buffalo vs Kansas City game belong as #1 on this list?