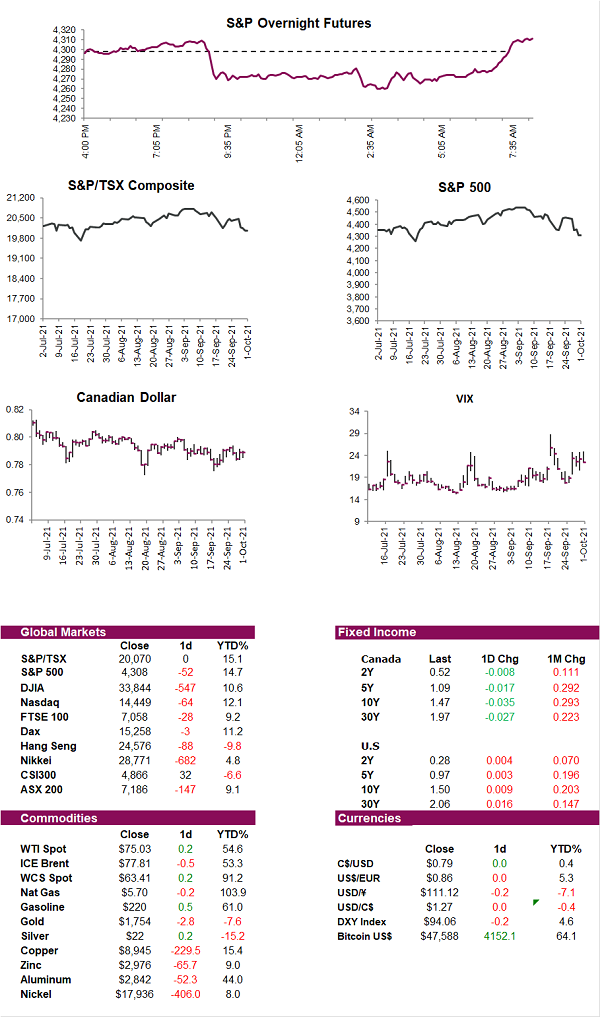

Today

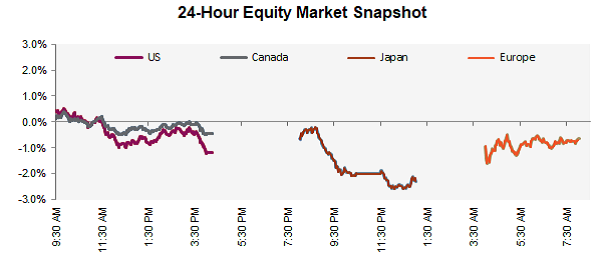

Futures are pointing to a weak open to kick off the third quarter as the risk-off tone continues with the “wall of worry” building in the US. After capping off a volatile month, investors remain on edge as inflation fears, slowing growth, and rising rates stay front of mind. The S&P 500 finished the month down -4.8%, breaking a seven-month winning streak while the Dow and Nasdaq both suffered its worst month of the year.

In a headline that reads like an Onion article, El Salvador just started mining bitcoin with volcanoes for the first time ever – and they’ve already made $269. President Nayib Bukele who has banked his political future on a nationwide bitcoin experiment tweeted early today that this is the country’s maiden voyage into volcano-powered bitcoin mining. He indicated that the mining project was still a work in progress and that they are in the process of “testing and installing” new mining equipment.

Airlines have been forced to adjust their business model since the beginning of the pandemic, and they have done that by making room in the middle. For decades, ferrying tourists to vacation destinations has helped major airlines cover basic costs, but the front of the plane is where they’ve racked up the bulk of their profits. But when the pandemic whacked business travel, carriers were left looking for another way to pad the bottom line and increasingly they’re finding it in the premium economy. Airlines have found that a number of leisure travelers are willing to splash out for a bit of extra elbow room at fares that are frequently more than double the cheapest economy seats.

While US legislators managed to get the debt ceiling debate pushed out to December, they continue to negotiate about a tax-and-spend package worth as much as $3.5 trillion. White House reps insist the deal is close, but this is President’s Biden’s first attempt at a substantial bi-partisan legislation and they will look pretty bad if it does not fly. The markets will love it if it passes. It is no secret to investors that fiscal spending came to the rescue over the past 18 months and much of it found its way eventually into housing, stocks and bonds. The debt it creates? That’s the kids’ problem!! YOLO!

Diversion: With the cold weather approaching and the golf season coming to an end, let’s watch one of the best holes in one ever.